Overview

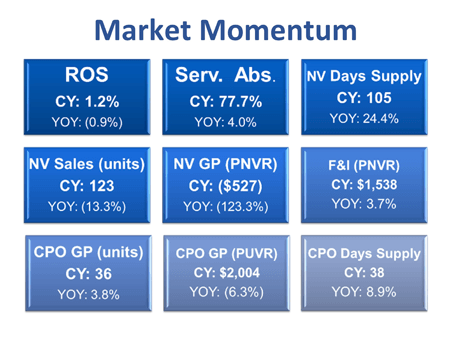

The 1st quarter of 2026 saw a significant drop in net profit from just a year ago. Dealership ROS fell to 1.2% down from 2.1% in Q1 ‘25. New vehicle sales decline combined with much lower gross profit margins contributed to the disappointing profit news. New vehicle gross profit contribution also fell sharply while pre-owned and aftersales rose and continued to carry the profit load for the dealers. Total operating expenses remained in check as dealers kept a lid on unnecessary expenses. Q1 saw the lost dealer count rise above 5% to 28% - too high to begin the new year. Last year's new vehicle buying frenzy in March ahead of heavy tariff threats can’t be overlooked as a significant reason why the YOY numbers were disappointing.

New-vehicle sales fell 13.3% year over year, while gross profit contribution from the department fell to below 15%. Front-end GPNVR of <$527> before bonus and F/I income only made things worse for the department. Q1 saw overall vehicle demand softened while EV business remained sluggish, and hybrid momentum strengthened as gas prices rose sharply. The result was that the new inventory days' supply rose to an unsettling 105 while the average new car price approached the $50k mark in Q1.

Consumers clearly shifted their attention away from new vehicle sticker shock and turned to used vehicles as pre-owned sales jumped 14.6% while CPO grew a steady 3.8%. Average pre-owned and CPO selling price remained virtually unchanged at $27k and $32k respectively. Customers continue to see the financial benefits of the strong CPO brand. Pre-owned days' supply fell almost 20% to 64 while CPO days' supply dropped to a very low 38 days. This pre-owned growth helped fuel internal sales in the shop, which improved in Q1.

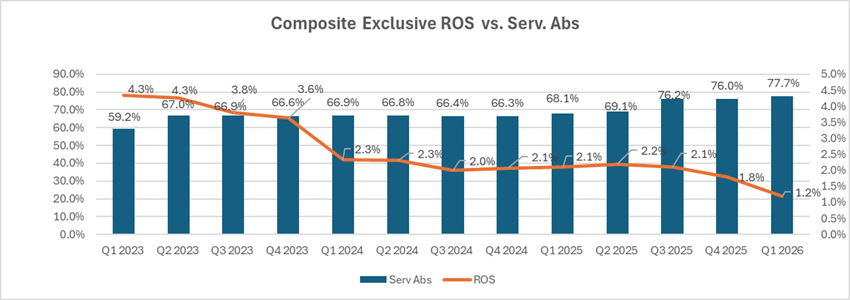

Fixed Operations continued to be the profit engine while reaching an impressive 77.7%, up from 73.8% last year. Service GP margin remained unchanged at a solid 77.4% while Parts GP margin rose to an impressive 42.6%. Warranty RO’s grew sharply and drove much of the fixed growth while Cust Pay and Internals showed modest growth in the shop. Total hours per RO fell slightly to 2.3 while Customer Pay fell to 2.0.

With Q1 ‘26 now in the rear-view mirror, dealers are looking forward to business growth based more on traditional consumer behavior and vehicle days' supply rather than geo-political policies that created so many highs and lows in ‘25. At least that is their hope!

New Vehicles

Q1 2026 continued the downward trend in New Vehicle sales and gross profit.

- Average new vehicle retail units show the sharpest YOY decline since 2020 at 13.3% from 142 to 123 units.

- Front-end GPNVR before bonus monies fell 123% YOY from <$236> to <$527> per unit.

- Total new-vehicle GPNVR including incentives and bonus fell 43.2% to $560 from $987 just a year ago.

- New vehicle days' supply rose by 24.4% to 105 days although still down from 121 days in Q4 ‘25.

- New vehicle advertising expense PNVR (net co-op) rose 48.7% to $821 per unit.

- F&I penetration increased to 155.8% while F&I GPNVR rose to $1,538.

- Dealership new vehicles transaction price rose slightly to $44.6K per unit.

As new vehicle demand softens, departments are facing real challenges in maintaining normal sales volume, reasonable GPNVR (before F/I) and keeping their days' supply in line to escape heavy floorplan costs. Dealers have increasingly relied on F&I and OEM support to offset these challenges. However, affordability pressure and high inventories could likely force dealers into even more aggressive pricing and lower margins in the months ahead.

Pre-Owned Vehicles

Pre-owned results were mixed as CPO sales were not as strong as non-CPO in 2025. This was due in large part to a low day's supply, which was just over half of the non-CPO inventory. The CPO brand continues to build loyalty, retention, aftersales profits, higher GPUVR and quicker turns, so dealers will need to find creative ways to build CPO stock. Finding more CPO appraisal opportunities should result in more CPO stock and therefore increased sales. For the CPO brand, it is not so much about managing the aged inventory as it is building stock levels sufficient for the market.

Pre-owned vehicle sales growth outperformed new vehicles in Q1 2026. Pre-owned retail and CPO sales showed positive gains, however, dealers sacrificed some gross profit margin to make that happen.

- Pre-owned retail sales rose 14.6%, while the CPO brand increased 3.8%

- Pre-owned front-end GPUVR dropped on average $140 (- 7%) to $1,775.

- Pre-owned reconditioning was virtually unchanged at $1,263 while CPO recon fell slightly to $1,581.

- The average pre-owned sales price held steady at $27,477 while CPO averaged $32,132 per unit indicating that the CPO brand remains strong with the excellent warranty coverage and improved reconditioning.

- Pre-owned-to-new sales ratio grew to a very impressive 1.1:1 helping build profits in all departments.

- Pre-owned F&I GPUVR rose a modest $31 to $683 in the 1st Qtr.

- Pre-owned days' supply dropped to a near perfect 64 days while CPO ended at a low 38 days' supply.

- Pre-owned yield (annualized total gross divided by average inventory investment) rose slightly to an impressive 65% indicating the overall pre-owned management process is improving.

Pre-owned department's gross profit contribution rose to 22% and well above the new car department as turn and GPUVR remained relatively strong for the dealerships. The focus moving forward will be building stock levels sufficient to meet ever-increasing demand, particularly in CPO which makes the most ROI but remains in very low days' supply. The dealership pre-owned process (recon days, turn, pricing, etc.) will need to be rock solid in order to trade for and purchase this incremental CPO stock.

Fixed Operations

Fixed Operations remained the key profit generator as absorption rose to a very impressive 77.7% in Q1. This can only happen with strong expense management (despite inflationary pressures) and a keen focus on driving service and parts sales in the shop. Dealerships showed remarkable flexibility in this area, and it signifies a positive direction for sustained profitability through ‘26.

- Total Service RO count grew 5.9% on the back of strong warranty RO growth of 15%

- Cust Pay Labor Sales/Gross Profit per RO remained virtually unchanged at $307 and $238 respectively

- Cust Pay Hours/RO fell from 2.1 to 2.0 hours in Q1

- Warranty Labor Sales/Gross Profit per RO remained unchanged at $306 and $250 respectively

- Internal Labor Sales/Gross Profit per RO grew 7.2% to $273 while Gross Profit per RO grew 6.4% to $202

- Total Labor Gross Profit per technician grew 6.9% to $19,851

- Parts RO Mech Sales per RO grew 2.7% from $197 to $203

- Parts Warranty Sales per RO declined 15.4% or $50 to $274 while Gross Profit per RO dropped to $124

- Parts Internal Sales/Gross Profit per RO were both down slightly at 1.6% and 2.2% respectively.

- Fixed absorption upward trend continued and grew from to 77.7%

Total service flat rate hours dropped over 31% YOY. This could indicate client retention numbers are falling. It will be important for dealers to manage the ever-growing ELRs to remain uber-competitive while at the same time ensuring shop hours are convenient to retain their valuable client base in the future.

Trends to Monitor

Below are key trends from our AMOS composite from all brands in US that Optimum continues to monitor closely:

- ROS has dropped to 1.2% as New Vehicle Sales and GPNVR dropped sharply in Q1 2026

- New vehicle floorplan remains a significant expense tied directly to turn and days' supply

- F/I continued to edge upward to help offset new sales volume and Front-End GPNVR

- Dealers are increasingly reliant on F&I, OEM bonuses, used vehicles and fixed operations to offset the weak profit contribution from the new vehicle department

- Used vehicle sales showed strong growth despite slightly lower GPUVR

- Fixed Operations are paying the bills and contributing ever more to the bottom line

- Parts turn improved slightly to over 6X annually

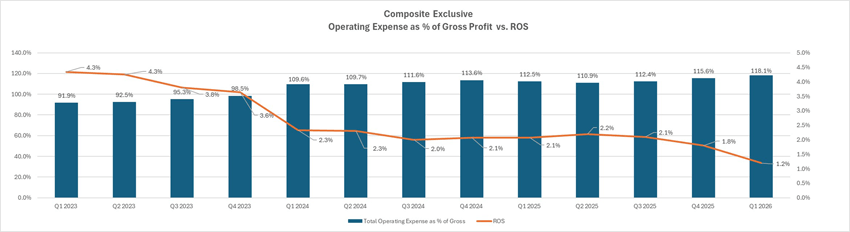

- Total operating expenses grew at a reasonable 5.8% but still too high for a strong ROS

Recommendations:

- Dealers and OEMS still need to find a balance between achieving sales targets and reasonable FE GPNVR in a market where new car margins continue to suffer

- Expense discipline will need to improve considerably in advertising, floorplan and personnel and AI may help in this area but it's too early to tell

- New Vehicle inventory turn will need to improve as both days' supply and floor plan costs have risen

- Finance Income’s role in new car profits will grow as dealers push for higher product penetration

- CPO brand growth will require full engagement by GM/DP to help build stocking levels to 60+ days

- Service departments will need to find new ways to entice more customers (CP RO count) to visit the shop without relying on so much pre-paid maintenance, warranty and higher labor rates

- A more consistent MPI process will be necessary to grow the much-needed shop hours

Q1 financial results suggest a very challenging road ahead for 2026 as ROS will need to rebound sharply for sustainability and future franchise investment. Dealers who can continue to lower operating expenses in key areas, build F/I, pre-owned and aftersales department sales will be in good shape to weather the bumpy road ahead. It's clear that the pre-COVID days of the daily grind of the retail car business are back and in full swing.

Note: All numbers mentioned above, except the ones specifically referenced, are based on a composite of all brands in the US using Optimum Info’s AMOS system (Audi, Hyundai, Kia, Mitsubishi, Volkswagen, and Volvo). The gathered data has been meticulously analyzed to provide accurate and comprehensive insights for the purpose of this article.