Overview

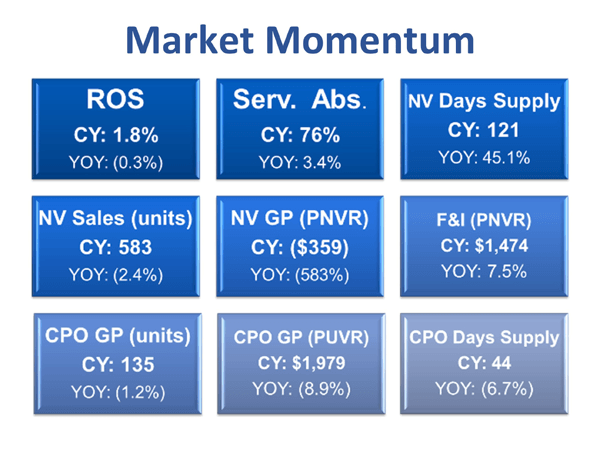

Despite the threat of ongoing tariffs, the end of EV tax credits and other economic and geo-political headwinds, 2025 shaped up to be a solid fiscal year for dealerships. Averaged ROS dropped slightly from 2.1% to 1.8%, resulting in a NBIT of $991k in ‘25. These results were due to continued erosion of new vehicle profits while growth in pre-owned, finance and aftersales departments helped close the year on a strong financial note. The loss dealer count (although still high) remained unchanged from a year ago at 24% while dealer balance sheets showed a healthy cash and NWC position showing they are well prepared financially for the upcoming year.

New vehicle sales fell a modest -2.4% to 583 as dealers fought to aggressively move units by year-end in hopes of achieving OEM sales bonuses and reducing floorplan expenses. In doing so, the new vehicle front-end GPNVR fell sharply to -$359 as competition grew. The F/I department helped cushion the blow as F/I GPNVR rose to a very respectable $1474. New vehicle inventories finished the year well above prior year levels at a 121 Days Supply as wholesale units jumped in the final quarter of the year combined with sluggish retail sales.

Pre-owned vehicle sales ended the year with strong momentum increasing just over 10% over 2024. Although CPO sales rose only slightly by 1.2% to 135 units, CPO font-end GPUVR ended the year just under the $2000 mark and along with its quick turn, provided a crucial profit center for the dealership operations. CPO inventory, unlike new vehicles, ended the year at a low 44 Days Supply.

Aftersales remained a bright spot in 2025 as profits from customer pay, warranty and internals all showed a nice uptick. The results helped grow aftersales absorption to a record of 76%. This is impressive as total expenses rose due to facility investments and pesky inflation. Aftersales highlights include a 10% growth in total service hours (CP, W, I) per RO to 2.2 and a .5% growth in internal RO’s indicating dealers are focused on MPI process and growing pre-owned.

Clearly, dealers have shown they remain remarkably flexible and adaptable in a volatile business environment. Recent changes to the BEV market and tariffs alone have required dealers (and OEM’s) to pivot on a moment’s notice. By driving pre-owned, finance and aftersales growth and at the same time keeping a watchful eye on operating expenses, dealers can look forward to continued financial success in 2026.

New Vehicles

The New vehicle department continued to struggle as sales volume dipped despite very strong advertising investment. The FE GPNVR fell by over 500% while the average sales price broke past the $44,000 mark. New inventory swelled to over a 100-day supply by year-end. F/I income of $1474 GPNVR and OEM monies helped prop up total GPNVR to a very modest $794 in 2025. Some key new vehicle highlights are below:

- New vehicle, including fleet and other franchise sales, declined 8.7% from 612 to 589.

- New vehicle average sales price rose slightly to $44,600.

- New Front-end GPNVR plummeted by 583% from a negligible -$53 to a loss of -$359 per unit.

- New Total GPNVR (including incentives/bonuses) fell by 30.8% to $794 as the department became increasingly reliant on F/I income and OEM bonus monies to make the department profitable.

- New vehicle days' supply surged 45.1% to 121 days despite the big uptick in advertising investment.

- New advertising expenditure rose 33% to $683 per unit as dealers made the final push to close out 2025.

- New F&I penetration increased to 157% while F/I GPNVR rose to a solid $1474.

Challenges remain in this department as achieving high sales volume will be critical to earning the OEM volume bonus monies needed to offset the eroding front-end gross profits. Dealers will likely struggle to find a good balance here. Also, dealers are becoming more relient than ever on the F/I department income and there is no foreseeable change in this trend. One added benefit of pursuing high volume sales targets at the risk of low front-end GPNVR is of course reducing high floorplan costs which will continue to drag down profits as interest rates remained stubbornly high.

Pre-Owned Vehicles

The pre-owned department, unlike their new vehicle counterpart, saw sales increase by 10% in 2025. This was due in large part to non-CPO sales as CPO sales grew only 1.2% in 2025. Pre-owned front-end GPUVR held steady at $1,820 while CPO fell just slightly to $1,979. Despite the modest growth in CPO sales, the higher GPUVR and quick turn meant customers still see significant value in the higher priced CPO brand. Reconditioning costs remained consistent while giving both service and parts much needed internal sales. Some key highlights are below:

- Pre-owned retail sales rose 10.1% while the CPO brand saw a modest 1.2% growth in 2025.

- Pre-owned front-end GPUVR was virtually unchanged at $1820 while CPO front-end GPUVR was $1979.

- Pre-owned recon cost rose 2.6% while CPO recon costs dropped 3.6%.

- Pre-owned average sales price remained unchanged at $27,723 while CPO was $32,689 per unit.

- Pre-owned to new ratio jumped 14.3% to 0.9 - ideal in today's market.

- Pre-owned F/I GPUVR rose a solid 23% to $673 in 2025.

- Pre-owned days' supply hit 75 while CPO ended 2025 with a much lower 44 days' supply.

- Pre-owned yield (annualized total gross / average inventory investment) fell 1% to a modest 34%.

Pre-owned results were mixed as CPO sales were not as strong as non-CPO in 2025. This was due in large part to a low day's supply, which was just over half of the non-CPO inventory. The CPO brand continues to build loyalty, retention, aftersales profits, higher GPUVR and quicker turns, so dealers will need to find creative ways to build CPO stock. Finding more CPO appraisal opportunities should result in more CPO stock and therefore increased sales. For the CPO brand, it is not so much about managing the aged inventory as it is building stock levels sufficient for the market.

Fixed Operations

Robust growth in service and parts drove a sizable part of the total profit generation in 2025 as fixed absorption hit a record of 76%. Service GP margin remained unchanged at a solid 77% while parts gross profit margin rose 0.5% to an impressive 42.1%. Service sales and gross profit in every repair order category also showed improvement year-over-year as customer pay, warranty and internals all had significant increases. Parts inventory turn jumped to 6.2 times annually from 5.9 a year ago.

- Cust Pay Labor Sales per RO was up 6.8% to $298 while Gross Profit per RO was up 6.9% to $231.

- Warranty Labor Sales per RO was up 10.2% to $290 while Gross Profit per RO moved up 10% to $235.

- Internal Labor Sales per RO grew 7% to $261 while Gross Profit per RO grew 6% to $194.

- Total Labor Gross Profit per technician grew an impressive 8% to $19,553.

- Parts Customer Pay (RO Mech) Sales per RO grew 6.7% from $186 to $199.

- Parts Warranty Sales per RO remained flat at $310 while Gross Profit per RO grew a modest 3% to $138.

- Parts Internal Sales and Gross Profit per RO were both down slightly at 1.9% and 1.1%, respectively.

- Service absorption upward trend continues and grows 4.6% to 76% up from 72.6% just a year ago.

Aftersales was a big highlight on many levels this year as sales in the shop and gross profit margins stayed exceptionally strong despite record high labor rates and parts pricing. All this is happening while RO counts have not really grown. As a result, aftersales departments will have to raise the bar and offer impeccable customer service to justify their ever-increasing ELR’s. In addition, building much needed internal sales will require an even stronger focus on pre-owned and CPO sales.

Trends to Monitor

Below are key trends from our AMOS composite from all brands in US that Optimum continues to monitor closely:

- New Vehicle sales slipped just 2.4% in 2025 while average days' supply shot up to 120 days.

- New front-end GPNVR fell sharply in 2025 as dealers chased OEM volume bonus sales targets.

- F/I income improved throughout 2025 helping to offset the front-end GPNVR shortfall.

- BEV demand fell sharply at the end of 2025 as losses on these vehicles were significant.

- Pre-owned sales grew 10% in 2025, yet CPO sales were stagnant as stock levels remain too low.

- The CPO Brand GPUVR was $1979 and exceeded all non-CPO sales and turn in pre-owned department.

- Aftersales played a big role in ROS as GP margins were excellent in service (77%) and parts (41%).

- Aftersales absorption jumped to 76% in 2025 as dealers focused heavily on this area of their business.

- Aftersales growth is the result of higher labor rates (ELR) not necessarily new clientele in the shop.

- Expense management was exceptional as dealers work diligently to keep operating expenses tight while fixed expenses climb from inflation and continued facility investment.

Recommendations:

- Dealers and OEMS need to find a balance between volume sales targets and reasonable FE GPNVR.

- New Vehicle inventory turn will need to improve as both days' supply and floor plan costs are high.

- Finance Income’s role in new car profits will grow as dealers push for higher product penetration.

- CPO growth will require building stock levels from higher trade ratios and more auction purchases.

- Service departments will need to find a way to entice more customers (grow RO count) to visit the shop without relying on so much pre-paid maintenance and higher labor rates.

- Service departments will need to re-evaluate technician current offerings and incentive programs when hiring young technicians today who's motivations are not just pay plan driven.

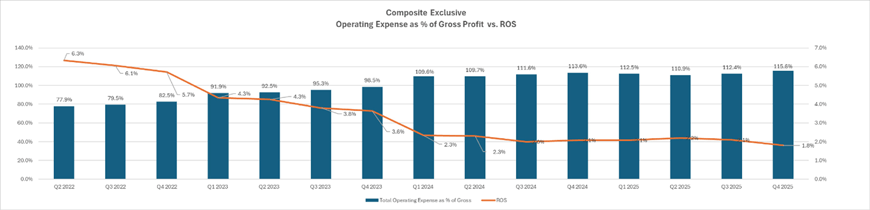

In summary, dealer profitability was solid in 2025, but business has certainly changed from just a few years ago. As the industry saw average new transaction price hit an eye watering $50,000-mark and gross profits continuing to erode, dealers found themselves focused on driving F/I, Pre-owned and Aftersales to bring ROS up to a more reasonable level. While these departments were driving profitability, the new vehicle department was facing a perfect storm of slowing sales, rising floorplan costs, and significantly lower margins. The new vehicle department's gross contribution fell sharply in 2025. In addition, COX Automotive found 21% of new car loans are now 84 months, and 1 in 5 customers have payments of $1000 per month. This trend not only pushes customers out of the retail market for years but also increases the likelihood of future loan defaults, not good news for dealers or customers. The Pre-owned department continued to chug along, supporting higher sales volume and solid GPUVR all while contributing more to the total gross profit of the dealership. Aftersales was the shining star for 2025 as absorption took center stage and helped carry much of the net profit in 2025.

Note: All numbers mentioned above, except the ones specifically referenced, are based on a composite of all brands in the US using Optimum Info’s AMOS system (Audi, Hyundai, Kia, Mitsubishi, Volkswagen, and Volvo). The gathered data has been meticulously analyzed to provide accurate and comprehensive insights for the purpose of this article.